In India, filing an Income Tax Return (ITR) forms an essential part of both personal and business finance management. Understanding ITR filing is important for all types of employees – salaried, business owners and freelancers – to comply with law and take advantage of financial perks.

Many people focus on the foundations, but there are some important areas in ITR that people tend to overlook such as picking the correct form, understanding the most recent tax law changes and knowing how certain income types affect you. It covers all aspects of crypto and more.

What Is ITR?

An Income Tax Return (ITR) is filled out by taxpayers to show their earnings, deductions, taxes paid and other financial matters to the Income Tax Department. It is required by the Income Tax Act, 1961 for every individual or organization earning taxable income in India to submit an annual return.

This process not only fulfills the rule of law but also shows how responsible you are with your finances and helps you in many ways. Submitting ITR has these benefits:

- Ensuring legal compliance

- Claiming refunds on excess tax paid

- Ensuring that I have documents to show my income for loan or visa processes

- Applying losses (business or capital) to future income

- Avoiding penalties and avoiding notices

Whether you’re handling this yourself or using itr filing services, it’s essential to understand what form you need and how to file it correctly.

Types of ITR Forms

Different taxpayers need to file different forms depending on their income sources, taxpayer category, and financial activities during the financial year. This is a list of the ITR types and the people or companies they cover:

ITR-1 (Sahaj)

- For people in India who earn a salary of up to ₹50 lakh.

- Consists of the wages, interest and benefits for owning one house property.

- None of these points are relevant for those who report capital gains, more than one property or foreign earnings.

ITR-2

- For individuals or HUFs without business/professional income

- This law is for those who have capital gains, multi-house properties or overseas assets.

ITR-3

- For people or HUFs with earnings from business or profession

- Required for freelancers, consultants, and partners in firms

ITR-4 (Sugam)

- If someone is applying presumptive income schemes stated in Sections 44AD, 44ADA or 44AE

- Applicable for small businesses and professionals with income up to ₹50 lakh

ITR-5, ITR-6, ITR-7

For LLPs, companies, trusts, and other legal entities

A professional itr consultant or tax file consultant can help choose the right form based on your income sources and compliance needs.

Common Mistakes to Avoid During ITR Filing

People with a lot of experience filing their taxes can still make mistakes. Such mistakes frequently cause taxpayers to receive notices, to owe interest or to have their returns turned down. These are the errors that happen most often:

- Picking the wrong Income Tax Return form

- Not checking that information matches on your AIS or Form 26AS

- Omitting to report your interest income or earnings from another source

- Failing to disclose foreign accounts (even those that are inactive)

- Not claiming big refunds under Section 80C or 80D

- Filing a tax return without linking Aadhaar to PAN.

Engaging professional tax consultancy services can help avoid these pitfalls, especially if you have multiple income sources, capital gains, or income from abroad.

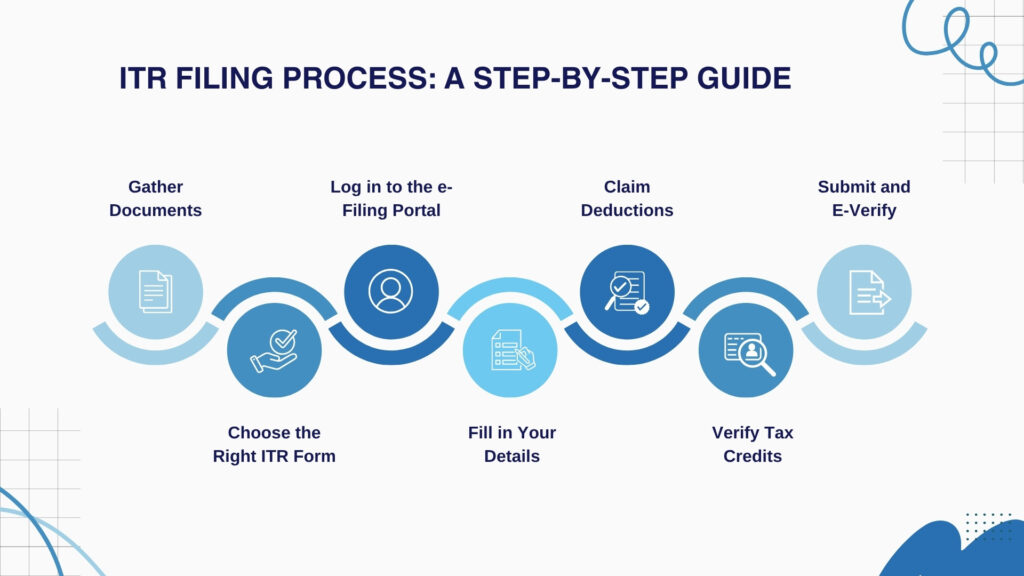

ITR Filing Process: A Step-by-Step Guide

Much of the process is now more accessible because of the online income tax portal. I can explain in detail how filing for divorce happens.

Step 1: Gather Documents

- Getting a PAN and an Aadhaar card

- A document from the employer called Form 16

- Form 26AS and AIS

- Account information and details on investments

- Backing paperwork for all your deducted expenses (insurance, ELSS, tuition fees, donations, etc.)

Step 2: Choose the Right ITR Form

Select the form based on your income type, as discussed earlier.

Step 3: Log in to the e-Filing Portal

Go to the official Income Tax website at www.incometax.gov.in and provide your PAN to sign in.

Step 4: Fill in Your Details

If you have pre-filled info from the portal, use that or manually enter your income, deductions and tax payments.

Step 5: Claim Deductions

Include those eligible expenses covered under Sections 80C to 80U to lessen the taxable amount.

Step 6: Verify Tax Credits

Check if the details from your tax calculation are the same as those in Form 26AS and AIS.

Step 7: Submit and E-Verify

Once validated, submit the form and complete the process with Aadhaar OTP, NetBanking, or offline verification.

A number of tax consultancy firms offer automated support or full-service help during this step for a hassle-free experience.

Overlooked but Essential Topics in ITR Filing

A lot of taxpayers fail to check for any special rules that may affect their returns. Here are some often-missed but important areas to note:

1. Capital Gains Report

Disclose accurately anything you earn from shares, mutual funds, property or cryptocurrency. The taxes on short-term and long-term gains are not the same. Usually, you must file ITR-2 or ITR-3 depending on the sort of gain you have.

2. Freelancers and Gig Workers

Freelancers, those running digital services and consultants are all considered to be self-employed. If your income reaches a certain amount, you may have to file ITR-3 instead of the presumptive scheme (ITR-4).

3. Filing for NRIs

NRIs frequently find it difficult to know if they are Indian residents for taxation purposes. Most people who have interest, property or capital gains income in India normally file ITR-2. An experienced tax consultant in India who is skilled in cross-country tax matters is preferred for applying the correct procedures.

4. Crypto and Virtual Digital Assets

As per new regulations, income from digital assets like Bitcoin or NFTs must be taxed at a flat 30% without deductions. A taxpayer needs to file using ITR-2 or ITR-3.

5. Clubbing of Income

Some parents put financial resources into their children’s names. Clubbing provisions can apply to the income that comes from such investments. Some people do not report this which may result in problems with compliance.

What If You File Late?

A penalty under Section 234F of up to ₹5,000 might be applied by the tax department if you miss the due date for filing your ITR (typically July 31 for individuals). In addition:

- You may lose the right to carry forward capital or business losses

- Interest may accrue on unpaid tax dues

- Getting refunds takes time.

- Rectifications take more time than regular checks do.

If you decide to do your taxes by yourself or with help, it’s very important to submit them before the deadline.

Tools You Should Know About

Before filing their return, taxpayers should go over the following two key resources:

Form 26AS

Here is your annual financial statement for tax purposes. It displays the tax collected at source (TDS), any prepaid taxes and so on.

AIS (Annual Information Statement)

AIS clearly separates your high-value transactions, showing mutual fund investments, property purchases and credit card expenses.

Always compare your ITR entries with these reports. If you’re unsure, a reliable income tax consultant can help reconcile and file accurately.

Tech Advancements in ITR Filing

The government has introduced several features to simplify and speed up the ITR process:

- Forms automatically completed using your PAN and Aadhaar.

- Verify your account fast using a one-time password (OTP).

- Bringing together AIS and TIS (Taxpayer Information Summary)

- AI is responsible for finding errors when they occur.

Although these new systems are helpful, complicated returns always need to be checked carefully. For this reason, lots of people continue using a tax consultant in India for specific advice.

FAQ’s

It ensures compliance, lets you claim refunds, carry forward losses, and improves loan and visa approvals. These are key benefits of filing ITR.

Types of ITR include ITR-1 to ITR-7. The right form depends on your income — salary, business, capital gains, or foreign income.

PAN, Aadhaar, Form 16, Form 26AS, bank statements, and investment proofs are required. ITR filing services can assist with this.

Yes, belated returns can be filed up to December 31 of the assessment year, but with a late fee of ₹1,000 to ₹5,000. However, delayed filing restricts certain benefits like loss carryforward and can lead to interest charges.